Industry overview

Ancillary revenue reached $62B in 2016 and projected to reach $180B in 2020

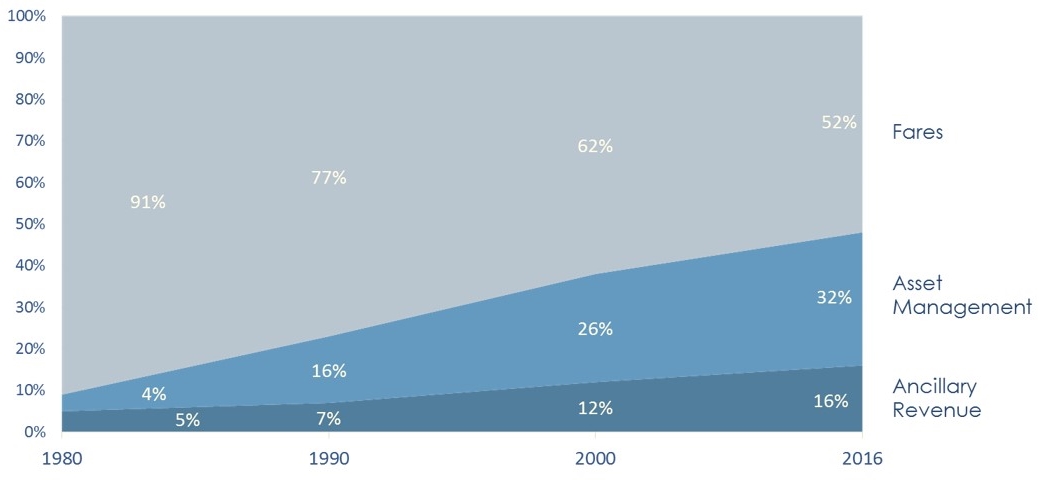

The Evolution Of The Airline Business Model

Legacy Carriers has dominated the Aviation market since last century and has since depended on the fares as their main source of revenue; with the entry of Low Cost Carriers a drastic change started to lure by stripping down the basic fare and offering ancillaries to make-up for the revenue along with a change in the route system and introducing new city pairs, all this was not enough until the financial system came in play to allow airlines change their asset management to a profit rather a liability in many different ways by deploying innovative asset funding instruments.

The global LCC sector has grown at a staggering pace since the beginning of this decade. There are now more than 100 LCCs operating a combined fleet of 6,000 aircraft and a doubled seat capacity reaching nearly 1.7 billion in 2018.

End result is a dramatic change in the revenue structure of Airlines; in 2016 returns generated from seat sales has shrunk to nearly 52%, allowing for greater revenue portions of ancillaries and asset management, 16% and 32% respectively.

It is estimated that $93 billion in flight and ancillary revenues will be recorded 2018 from 4.3 billion departing traveler hence providing airlines with a golden opportunity to build and strengthen their revenue structure and customer experience in the short-term.

Source: The 2018 of Ancillary Revenue by IdeaWorksCompany + apps analysis

Source: The 2018 of Ancillary Revenue by IdeaWorksCompany + apps analysis

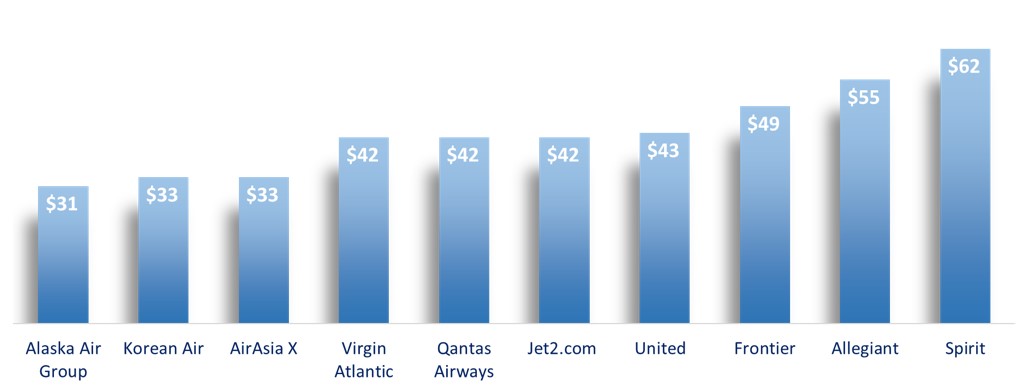

Ancillary Revenue per Carried Passenger

Ancillary revenue as a portion of total revenue appears to have reached a ceiling of 50% with the top producer being Spirit at 46.6 percent. Michael O’Leary has remarked throughout his tenure as CEO of Ryanair that fares could someday be zero; consumer air travel cost would be limited to a la carte fees and other ancillary revenue. Over time, that objective eluded Ryanair, with other airlines doing much better. Spirit’s total ticket revenue was approximately $110 per passenger for 2017. Of this amount, about $62 (or 56.3 percent) would qualify as ancillary revenue.

The top performing airlines are largely low cost carriers, with a couple of global network airlines appearing, when ancillary revenue is expressed on a per passenger basis (Chart on the right). Top producers, from various ancillary revenue sources, by global region are: Spirit $62, Allegiant $55, and Frontier $49. The definition of ancillary revenue includes the results produced by a carrier’s frequent flyer program and this can provide a substantial benefit for global airlines such as Qantas and United. For Qantas, a perennial best performer on this list, its loyalty segment achieved revenue in excess of AUD $1.5 billion (nearly $1.16 billion) for fiscal year 2017. That’s a stunning $98 per member or almost $42 per passenger.

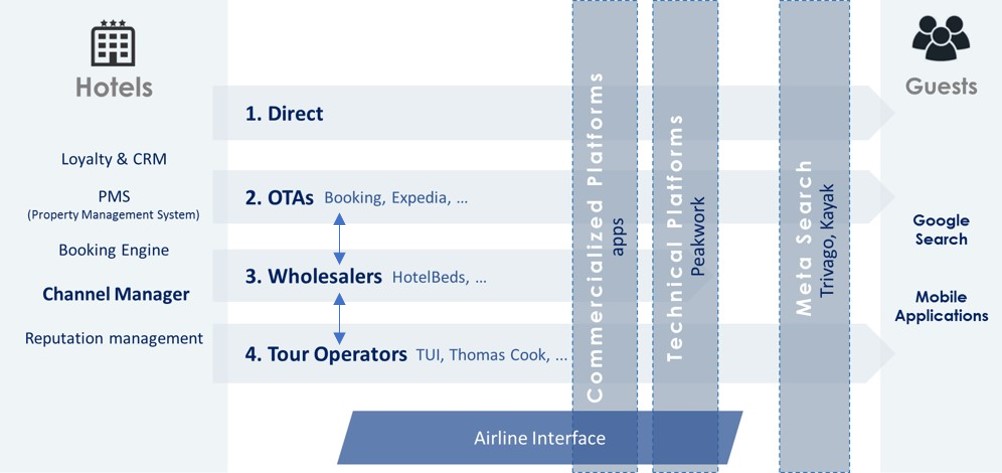

Hotel Distribution Chain & The Airline Edge

During decades the travel industry in general and the hotel industry in specific has been struggling to reach customers through B2B and B2C networks. With the internet and advanced reservation technologies entering the scene coupled with ever growing payment channels the marketing scene entered an ever-progressive trance to create multiple players other than the existing classic channels.

Major Hotels nowadays have deployed sophisticated reservation and intelligence systems to protect their interest and has opened distribution various channels, each with different combinations of ‘connections’ to deliver a final reservation to the guest.

Guests on the other hand have a wide range of choices to ultimately decide their preference.

While wholesalers positioned themselves as the "friendly enemies" securing occupation levels to hotels, OTA's are spending Billions on google marketing to reach the end user at his finger tips and meta-searchers squeezing their way in between Airlines are emerging to the scene with a new dimension.

Airlines are convinced that they are the first stop shop in the travel decision journey and with the abundance of empty seats could offer combined packages at the lowest possible value to finally become the one stop shop selling all travel services to the their passengers.

Achieving such position does not come cheap although with Airlines requiring a full holiday arm setup to offer such store front at lowest price and at this point only commercialized e-travel platforms kicks in with a plug and play solution. Along the past 10 years such low investment solution has proved to yield the highest conversion rates hence lucrative ancillary revenues to Airlines.

Source: Dealroom.co - Online Travel Report